Page 18-12

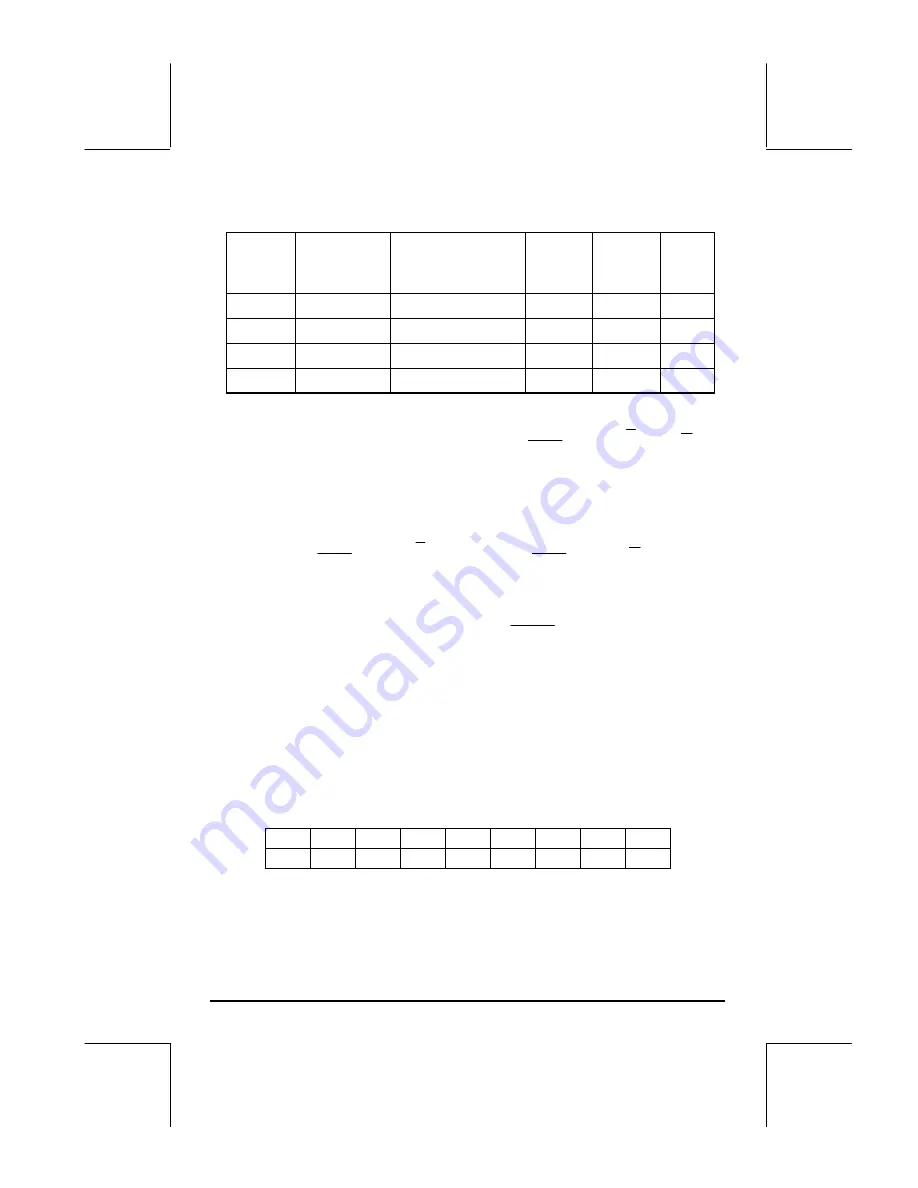

Indep.

Depend.

Type of

Actual

Linearized

variable

Variable Covar.

Fitting Model

Model

ξ η

s

ξη

Linear

y = a + bx

[same]

x

y

s

xy

Log.

y = a + b ln(x)

[same]

ln(x)

y

s

ln(x),y

Exp.

y = a e

bx

ln(y) = ln(a) + bx

x

ln(y)

s

x,ln(y)

Power

y = a x

b

ln(y) = ln(a) + b ln(x)

ln(x)

ln(y)

s

ln(x),ln(y)

The sample covariance of

ξ,η

is given by

)

)(

(

1

1

η

η

ξ

ξ

ξη

−

−

−

=

∑

i

i

n

s

Also, we define the sample variances of

ξ

and

η

, respectively, as

2

1

2

)

(

1

1

ξ

ξ

ξ

−

−

=

∑

=

n

i

i

n

s

2

1

2

)

(

1

1

η

η

η

−

−

=

∑

=

n

i

i

n

s

The sample correlation coefficient r

ξη

is

η

ξ

ξη

ξη

s

s

s

r

⋅

=

The general form of the regression equation is

η

= A + B

ξ

.

Best data fitting

The calculator can determine which one of its linear or linearized relationship

offers the best fitting for a set of (x,y) data points. We will illustrate the use of

this feature with an example. Suppose you want to find which one of the data

fitting functions provides the best fit for the following data:

First, enter the data as a matrix, either by using the Matrix Writer and

entering the data, or by entering two lists of data corresponding to x and y

and using

x 0.2 0.5 1 1.5 2 4 5 10

y 3.16 2.73 2.12 1.65 1.29 0.47 0.29 0.01